Mutual Funds

>>

Concept of Mutual Funds

>>

History of Indian Mutual Fund Industry

>>

Organization of a Mutual Fund

>>

Types of Mutual Fund Schemes

>>

Advantages of Mutual Funds

>>

Mutual Fund Terminology

Concept of Mutual Funds (Back To Top)

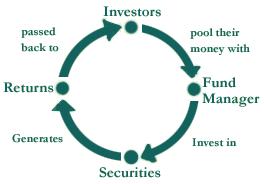

A Mutual Fund is a trust that pools the savings of a number of investors who share a common financial goal. The money thus collected is then invested in capital market instruments such as shares, debentures and other securities. The income earned through these investments and the capital appreciation realized are shared by its unit holders in proportion to the number of units owned by them. Thus a Mutual Fund is the most suitable investment for the common man as it offers an opportunity to invest in a diversified, professionally managed basket of securities at a relatively low cost. The flow chart below describes broadly the working of a mutual fund

History of Indian Mutual Fund Industry (Back To Top)

The mutual fund industry in India started in 1963 with the formation of Unit Trust of India, at the initiative of the Government of India and Reserve Bank of India. The history of mutual funds in India can be broadly divided into four distinct phases

First Phase - 1964-87

Unit Trust of India (UTI) was established on 1963 by an Act of Parliament. It was set up by the Reserve Bank of India and functioned under the Regulatory and administrative control of the Reserve Bank of India. In 1978 UTI was de-linked from the RBI and the Industrial Development Bank of India (IDBI) took over the regulatory and administrative control in place of RBI. The first scheme launched by UTI was Unit Scheme 1964. At the end of 1988 UTI had Rs.6,700 crores of assets under management.

Second Phase - 1987-1993 (Entry of Public Sector Funds)

1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks and Life Insurance Corporation of India (LIC) and General Insurance Corporation of India (GIC). SBI Mutual Fund was the first non- UTI Mutual Fund established in June 1987 followed by Canbank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89), Indian Bank Mutual Fund (Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund (Oct 92). LIC established its mutual fund in June 1989 while GIC had set up its mutual fund in December 1990.

At the end of 1993, the mutual fund industry had assets under management of Rs.47,004 crores.

Third Phase - 1993-2003 (Entry of Private Sector Funds)

With the entry of private sector funds in 1993, a new era started in the Indian mutual fund industry, giving the Indian investors a wider choice of fund families. Also, 1993 was the year in which the first Mutual Fund Regulations came into being, under which all mutual funds, except UTI were to be registered and governed. The erstwhile Kothari Pioneer (now merged with Franklin Templeton) was the first private sector mutual fund registered in July 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and revised Mutual Fund Regulations in 1996. The industry now functions under the SEBI (Mutual Fund) Regulations 1996.

The number of mutual fund houses went on increasing, with many foreign mutual funds setting up funds in India and also the industry has witnessed several mergers and acquisitions. As at the end of January 2003, there were 33 mutual funds with total assets of Rs. 1,21,805 crores. The Unit Trust of India with Rs.44,541 crores of assets under management was way ahead of other mutual funds.

Fourth Phase - since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI was bifurcated into two separate entities. One is the Specified Undertaking of the Unit Trust of India with assets under management of Rs.29,835 crores as at the end of January 2003, representing broadly, the assets of US 64 scheme, assured return and certain other schemes. The Specified Undertaking of Unit Trust of India, functioning under an administrator and under the rules framed by Government of India and does not come under the purview of the Mutual Fund Regulations.

The second is the UTI Mutual Fund, sponsored by SBI, PNB, BOB and LIC. It is registered with SEBI and functions under the Mutual Fund Regulations. With the bifurcation of the erstwhile UTI which had in March 2000 more than Rs.76,000 crores of assets under management and with the setting up of a UTI Mutual Fund, conforming to the SEBI Mutual Fund Regulations, and with recent mergers taking place among different private sector funds, the mutual fund industry has entered its current phase of consolidation and growth.

The graph indicates the growth of assets over the years.

Organization of a Mutual Fund (Back To Top)

There are many entities involved and the diagram below illustrates the organizational set up of a mutual fund:

Types of Mutual Fund Schemes (Back To Top)

There are a wide variety of Mutual Fund schemes that cater to your needs, whatever your age, financial position, risk tolerance and return expectations.

By Structure

- Open Ended Schemes: An open-end fund is one that is available for subscription all through the year. These do not have a fixed maturity. Investors can conveniently buy and sell units at Net Asset Value ("NAV") related prices. The key feature of open-end schemes is liquidity.

- Closed Ended Schemes: These funds have a pre-specified maturity period. The 'Unit Capital' of such schemes is fixed as it makes a onetime sale of a fixed number of units. After the offer closes, closed ended funds do not allow investors to buy or redeem units directly from funds.

- Interval Schemes: These combine the features of open-ended and close-ended schemes. They may be traded on the stock exchange or may be open for sale or redemption during predetermined intervals at NAV related prices.

By Nature

- Equity funds:

These funds invest a maximum part of their corpus into equities. The structure of the fund may vary different for different schemes and the fund manager's outlook on different stocks. The Equity Funds are sub-classified depending upon their investment objective, as follows:

- Diversified Equity Funds

- Mid-Cap Funds

- Sector Specific Funds

- Tax Savings Funds (ELSS)

- Equity investments are meant for a longer time horizon, thus Equity funds rank high on the risk-return matrix.

- Debt funds:

The objective of these Funds is to invest in debt papers. Government authorities, private companies, banks and financial institutions are some of the major issuers of debt papers. By investing in debt instruments, these funds ensure low risk and provide stable income to the investors. Debt funds are further classified as:

- Gilt Funds:

Invest their corpus in securities issued by Government of India, popularly known as "Gilts". These Funds carry zero default risk but are associated with interest rate risk. These schemes are safer as they invest in papers backed by Government.

- Gilt Funds:

Invest their corpus in securities issued by Government of India, popularly known as "Gilts". These Funds carry zero default risk but are associated with interest rate risk. These schemes are safer as they invest in papers backed by Government.

- Income Funds:

Invest a major portion into various debt instruments such as bonds, corporate debentures and government securities.

- Monthly Income Plans (MIPs):

Invests maximum of their total corpus in debt instruments while they take minimum exposure in equities. It gets benefit of both equity and debt market. These scheme ranks slightly high on the risk-return matrix when compared with other debt schemes.

- Short Term Plans (STPs):

Meant for investment horizon for three to six months. These funds primarily invest in short term papers like Certificate of Deposits (CDs) and Commercial Papers (CPs). Some portion of the corpus is also invested in corporate debentures.

- Liquid Funds:

Also known as Money Market Schemes, these funds provide easy liquidity and preservation of capital. These schemes invest in short-term instruments like Treasury Bills, inter-bank call money market, CPs and CDs. These funds are meant for short-term cash management with an investment horizon of 1day to 3 months. These schemes are considered to be the safest amongst all categories of mutual funds.

- Balanced funds:

As the name suggest they, are a mix of both equity and debt funds. They invest in both equities and fixed income securities, which are in line with pre-defined investment objective of the scheme. These schemes aim to provide investors with the best of both the worlds. Equity part provides growth and the debt part provides stability in returns.

By Investment Objective

- Growth Schemes: Aims to provide capital appreciation over the medium to long term. These schemes normally invest a majority of their funds in equities and are willing to bear short term decline in value for possible future appreciation.

- Dividend/Income Schemes: Aim to provide regular and steady income to investors. These schemes generally invest in fixed income securities such as bonds and corporate debentures. Capital appreciation in such schemes may be limited.

- Balanced Schemes: Aim to provide both growth and income by periodically distributing a part of the income and capital gains they earn. They invest in both shares and fixed income securities in the proportion indicated in their offer documents.

- Money Market / Liquid Schemes: Aim to provide easy liquidity, preservation of capital and moderate income. These schemes generally invest in safer, short term instruments such as treasury bills, certificates of deposit, commercial paper and interbank call money.

Other Equity related Schemes

- Tax Saving Schemes: Tax-saving schemes offer tax rebates to the investors under tax laws prescribed from time to time. Under Sec.88 of the Income Tax Act, contributions made to any Equity Linked Savings Scheme (ELSS) are eligible for rebate.

- Index Schemes: Index schemes attempt to replicate the performance of a particular index such as the BSE Sensex or the NSE Nifty. The portfolio of these schemes will consist of only those stocks that constitute the index, and with the same weightage as in the index it replicates. Hence, the returns from such schemes would be more or less equivalent to those of the index it replicates.

- Sector Specific Schemes: These schemes invest in the securities of specific sectors, e.g. Pharmaceuticals, Software, Fast Moving Consumer Goods (FMCG), Petroleum stocks, etc. The returns in these funds are dependent on the performance of the respective sectors/industries.

- Fund of Funds: As the name suggests, these Mutual funds invest in other mutual fund schemes offered by different AMCs. Fund of Funds maintain a portfolio comprising of units of other mutual fund schemes.

Advantages of Mutual Funds (Back To Top)

Portfolio Diversification: Mutual funds are a convenient and affordable way of investing in a wide range of investments which would be very difficult and time-consuming to purchase and manage individually. Mutual funds typically invest in a broad cross-section of industries and sectors, and thereby offer a degree of diversification that would be difficult to achieve on your own.

Professional management: Mutual Funds appoint experienced, professional Fund Managers who devote themselves exclusively to tracking the markets, analyzing securities and implementing a consistent investment strategy. The Fund Managers are backed by dedicated Research Teams, who actively analyze the overall market conditions as well as individual securities and assist the Fund Manager in selecting the best opportunities for investment

Flexibility: Mutual Funds employing a variety of investment strategies are available to help meet the needs of every type of investor, from conservative to very aggressive.

Also, through features such as Systematic Investment Plans (SIP), Systematic Transfer Plans (STP), Systematic Withdrawal Plans (SWP) and dividend reinvestment plans; you can systematically invest or withdraw funds according to your needs and convenience.

Hassle-free Administration: Investing in a Mutual Fund reduces paperwork and helps avoid many problems such as bad deliveries, delayed payments and unnecessary follow up with brokers and companies. Moreover, you can track your portfolio online - anywhere, anytime.

Sound Returns: A well-selected portfolio of Mutual Funds has the potential to deliver satisfactory returns over the medium to long term, with low volatility.

Transparency: Regular information on the value of your investment in addition to disclosure on the specific investments made by your scheme, the proportion invested in each class of assets and the fund manager's investment strategy and outlook, is provided by each Mutual Fund.

Well-Regulated: All Mutual Funds are registered with SEBI and they function within the limits of strict regulations designed to protect the interests of investors. Also the Association of Mutual Funds in India (AMFI) reassures the investors in units of mutual funds that the mutual funds function within the strict regulatory framework.

Mutual Fund Terminology (Back To Top)

Net Asset Value (NAV)

Net Asset Value (NAV) is a term used to describe the value of an entity's assets less the value of its liabilities. The term is commonly used in relation to collective investment schemes. For Mutual Fund Schemes, the NAV is the total value of the fund's portfolio less its liabilities. Its liabilities may be money owed to lending banks or fees owed to investment managers.

Assets under Management (AUM)

In general, the market value of assets an investment company manages on behalf of investors. There are widely differing views on what the term means. Some financial institutions include bank deposits, mutual funds and institutional money in their calculations. Others limit it to funds under discretionary management where the client delegates responsibility to the company.

Units

A Mutual Fund unit is what individual investors buy which gives them a "pro rata" share of the value of the investments of the fund. The unit value of the fund is struck by adding up the values of all the investments at their market prices, subtracting amounts owed by the fund and dividing by the number of units held.

New Fund Offer (NFO)

A NFO is a security offering in which investors can purchase units of a Mutual Fund. A new fund offer occurs when a mutual fund is launched, allowing the firm to raise capital for purchasing securities. A new fund offer is similar to an initial public offering. Both represent attempts to raise capital to further operations.

Entry / Exit Load

Mutual Fund Companies incur some expenses to float a fund and also they have many administrative and operative expenses. So to meet those expenses they collect a percentage of fees from the investors, which are called loads. If they collect the fee when you buy the units, then it is called as entry load. If they charge that fee when you sell your units back to them then it is called as exit load.

Diversification

Diversification is a risk management technique, related to hedging, that mixes a wide variety of investments within a portfolio. Diversification minimizes the risk from any one investment. It strives to smooth out unsystematic risk events in a portfolio so that the positive performance of some investments will neutralize the negative performance of others.

Fund Manager

The person(s) responsible for implementing a fund's investing strategy and managing its portfolio trading activities. A fund can be managed by one person, by two people as co-managers and by a team of three or more people. Fund managers are paid a fee for their work, which is a percentage of the fund's average assets under management.

Asset Allocation

Asset allocation is a term used to refer to how an investor distributes his or her investments among various classes of investment vehicles. A large part of financial planning is finding an asset allocation that is appropriate for a given person in terms of their appetite for and ability to shoulder risk. Examples of various asset classes are: Equity, Bonds, Fixed Deposits, Real Estate, Cash, etc.